Every Lender Replaces Their LMS Eventually

Five symptoms tell you whether you replace your LMS on your terms — or the board's. Three or more on the table is a board-level risk, not an IT one to defer.

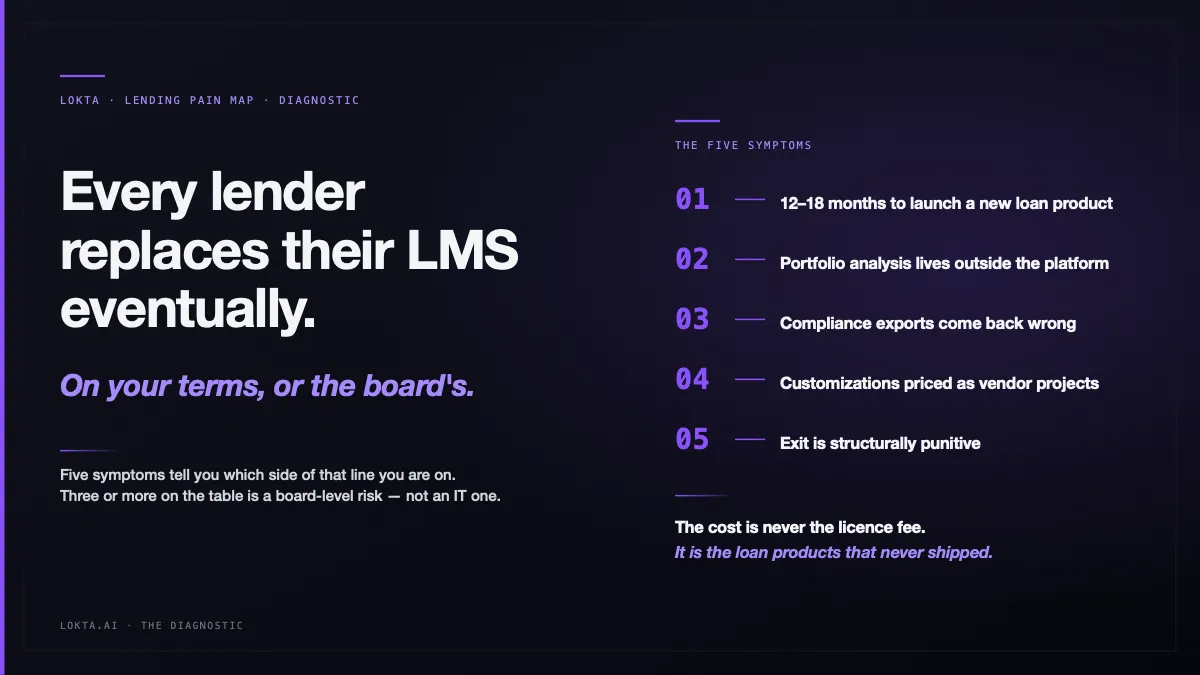

Every lender replaces their LMS eventually. The only question is whether you do it on your terms — or the board’s.

By the time the board names the platform as the problem, the timeline is no longer yours.

Five symptoms tell you which side of that line you are on. Three or more on the table is a board-level risk item — not an IT one. Here is the diagnostic.

1. A new loan product takes 12 to 18 months to launch

Traditional platforms take 12–18 months to launch new loan products.

Modern lending-native architectures ship a new loan product in weeks. The gap is not effort. It is who is allowed to reshape the product configuration.

On a legacy LMS, every change to the product structure — interest method, charges, repayment frequency, cohort eligibility, NPA buckets — flows through the vendor as a configuration request, a roadmap line item, or in the worst case a Statement of Work. The lender’s product team becomes a requirements-gatherer; the vendor’s services arm holds the keys. Multiply that bottleneck by the three-to-five product launches a competitive lender wants per year, and the math works out to a permanent capacity gap against fintechs and AI-native lenders who configure in their own UI and ship in days.

The board reads this as: “We cannot move at market speed.” That reading is correct.

2. Every meaningful portfolio analysis happens outside the platform

All analysis has to be done in other applications. The ability to build custom reports inside the platform would be beneficial.

This is not a reporting inconvenience. It is an unauditable layer between the system of record and every executive decision that depends on it.

When the board reviews delinquency trends, the answer comes from a spreadsheet built off an export. When the regulator asks for the methodology behind a provision, the methodology lives in a different spreadsheet. When the AI ambition arrives — “let’s use ML for early-warning signals on the book” — the foundation is data that left the system and got reshaped by hand. Every analytical output is one degree separated from the audited core. The deeper pattern behind this symptom — why lender portfolio analytics lives in Excel — is structural, not a reporting gap.

For a board considering AI-readiness, the question is not “Can we add AI to our LMS?” It is “Are we even working off the same numbers our system of record holds?“

3. Compliance exports come back wrong, and the vendor cannot fix them

HMDA exports are “in some cases incorrect,” and the HMDA screen “cannot be changed.”

When regulator-grade evidence depends on parallel spreadsheets, the LMS has stopped being a system of record and become an exhibit.

Every regulator publishes filing formats — HMDA in the United States, the RBI’s monthly returns in India, the FCA’s regulatory return suites in the UK. The lender carries the legal obligation; the LMS vendor implements the export. When the implementation is wrong and the vendor will not change it, three things happen at once: a parallel reconciliation process springs up (a person with a spreadsheet and the patience to do this every quarter), the auditable trail forks (the system says one number, the filing says another), and the next regulator exam costs days of rework. None of those costs sit on the LMS budget line. They sit on operations, on compliance, and on counsel — until someone adds them up and walks them into the audit committee.

4. Every customization is priced as a vendor project

Modifications requiring extensive project engagement, even for minor adjustments.

— Reviewers of the dominant commercial banking LOS, on Software Advice

Over a five-year contract, the lender’s own roadmap becomes a line item in the vendor’s services revenue.

This is the most measurable of the five. Pull up the last three years of services invoices. Add up what the lender paid the vendor for changes the in-house team described as “business as usual” — a new charge type, a tweaked schedule allocation, a regulator-driven field. That total is a contracted-in tax on product velocity. The legacy LMS contract is rarely a software contract; it is a software-and-services contract where the services arm is the actual business. The architectural pattern behind this dynamic is the LMS customization trap — why every non-standard need becomes a priced engagement.

5. Exit is structurally punitive

Vendors with exclusivity clauses may need to pay 50%, 80%, or even 100% of the remaining contract value to exit the service.

The exit clause is what makes the other four symptoms strategic.

Without an exit clause, an LMS that ships product slowly, hides analytics, breaks compliance, and prices customizations as projects is annoying — but you can leave at the next renewal. With an exclusivity or punitive-exit clause, every one of those problems compounds because the lender cannot walk away. The vendor has priced the lender’s patience.

The negotiation moment is at the next renewal, before the next exclusivity term locks in. The board needs to ask whether the renewal was actually a renewal — or a fresh strategic commitment by another name.

The cost is the loan products that never shipped

The cost of a strategic-liability LMS is never the licence fee. It is the loan products that never shipped, the portfolio insights that arrived a quarter late, the compliance exposure no one reconciled, the customizations the vendor priced as projects, and the renewal year that arrived without options.

Three or more of these symptoms on the table is a board-level risk item, not an IT one. Lenders who run this diagnostic on their own terms — before the board does it for them — replace the LMS on a clean schedule, with a competitive bidding process and a real budget. Lenders who wait get one offer, one timeline, and one quarter to decide.

The replacement is not the question. It happens to every lender. The only question on the table is who controls the timeline.

Read next: The Lending Technology Pain Map (long-form dossier) — the audience-by-audience analysis of how loan officers, in-house tech teams, and executives describe the same platform in three different vocabularies. The dossier explains the territory; this diagnostic gives you the test. When the diagnostic says replace, the LMS RFP toolkit is the vendor-neutral kit for running the selection.

Frequently asked questions

When does an LMS become a board-level risk rather than an IT issue?

When three or more of the diagnostic symptoms are on the table simultaneously: 12-18 month time-to-market for new loan products, portfolio analytics that live outside the platform, compliance exports the vendor cannot fix, customizations priced as services projects, and structurally punitive exit clauses. Any one of these is an IT inconvenience. Three or more compound into a strategic constraint on what the lender can ship and how fast — which is a board concern, not a CIO line item.

What is a ‘strategic-liability LMS’?

A loan management system whose architecture, contract terms, and vendor relationship together prevent the lender from making the product, compliance, and exit decisions a board would otherwise expect to make. The licence fee is rarely the issue. The cost surfaces as loan products that took 18 months to launch, portfolio insights that arrived a quarter late, regulatory exposure no one reconciled, and renewal years that arrived without options.

What does an exit penalty look like on a typical LMS contract?

Exclusivity and minimum-spend clauses can require the lender to pay 50%, 80%, or even 100% of the remaining contract value to leave the service. The exit clause is what makes the other four symptoms strategic — without it, an LMS that ships product slowly and prices customizations as projects is annoying but escapable at the next renewal. With it, every problem compounds because the lender cannot walk away. The negotiation moment is at the next renewal, before another exclusivity term locks in.

Why is this a different question from a standard vendor evaluation?

A vendor evaluation asks: does this platform meet our requirements? The five-symptom diagnostic asks the prior question: has our current platform crossed from operational drag into strategic liability? The two evaluations sit in different rooms — one is procurement, the other is the board. Lenders who run the diagnostic on their own terms replace the LMS on a clean schedule with a competitive process. Lenders who wait for the board to surface the question replace it on the board’s timeline, with one vendor, one number, and one quarter to decide.