How to Use AI Agents in Loan Servicing

Loan servicing in plain terms, the ten categories of servicing tickets, and which ones an AI agent can run end to end today — plus the deployment playbook.

Most “AI in loan servicing” content jumps straight to “we automated collections” without first defining what loan servicing actually covers. The result is recommendations that sound right and don’t survive contact with an actual servicing operation.

This post starts at the bottom. What is loan servicing, what kinds of tickets arrive in a servicing operation, and which of those tickets an AI agent can actually run today — with the deployment playbook for getting there without breaking trust.

What is loan servicing?

Loan servicing is the operational layer of lending that runs from the moment a loan is disbursed until it is closed — paid off, foreclosed, written off, or settled. It is the longest phase of the loan lifecycle, typically 90–99% of the loan’s calendar life, and the phase where the lender’s economics actually realise: interest accrues, principal returns, defaults emerge, operational cost compounds.

Concretely, servicing covers everything that happens after the Loan Origination System hands the loan to the Loan Management System (Lokta’s origination is the Loan Origination System, which disburses cleanly into the LMS on a shared canonical model). Schedule generation, repayment processing, interest calculation, charge application, communication with the borrower, hardship handling, collections, NPA classification, regulatory reporting, complaint resolution, lifecycle events such as top-ups and closures, and the audit trail behind every state change.

Servicing is mostly silent and slow when nothing is going wrong, and intense when something is. The job of a servicing operation is to handle both modes well — at scale, on time, inside policy, with an audit trail. AI helps in the same place a good operations team would help: not by inventing new categories of work, but by absorbing the volume in the categories that already exist.

What lands on a servicing team’s desk

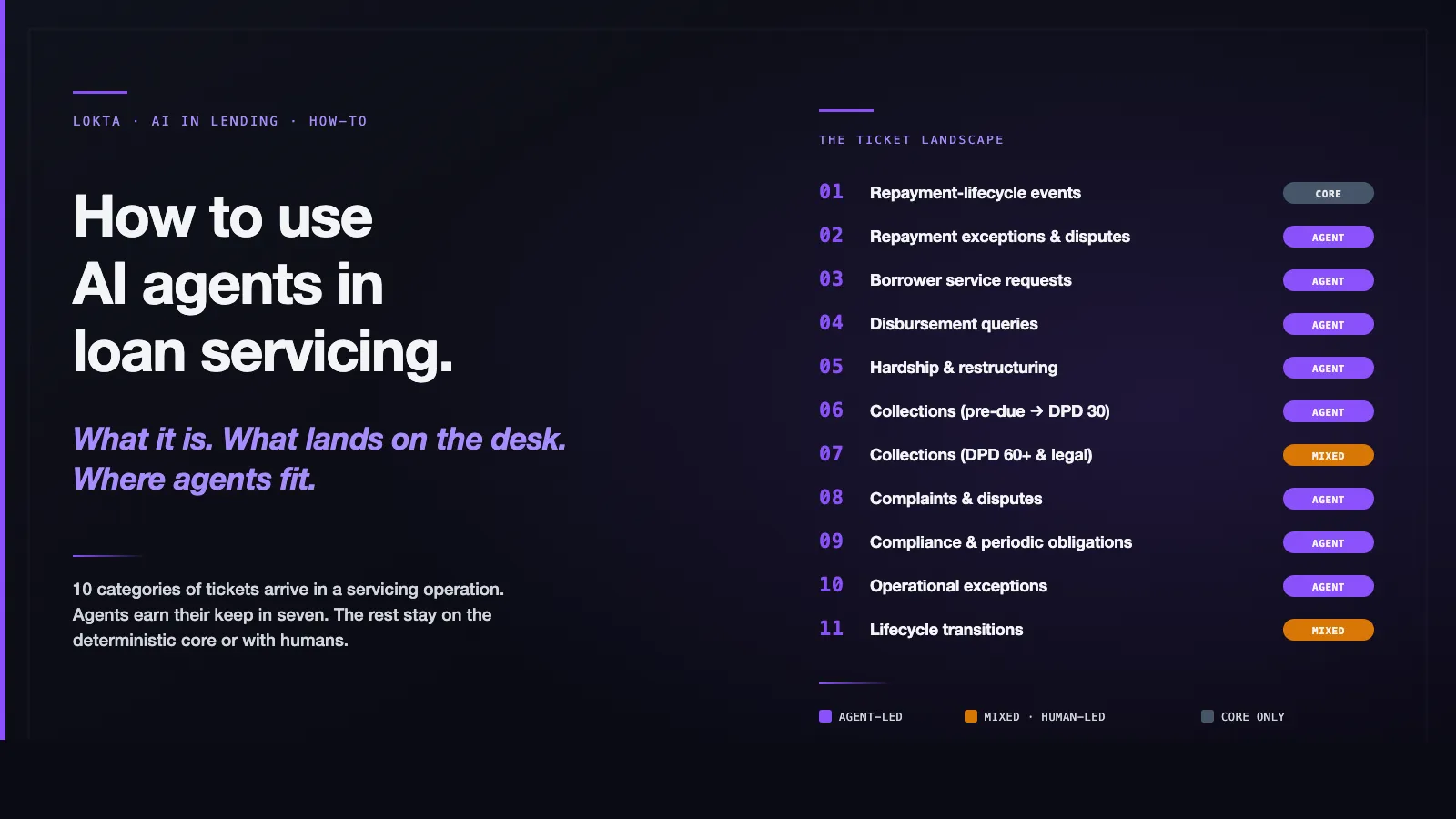

Ten categories of tickets arrive at a servicing operation. The volumes vary by lender — a microfinance NBFC’s mix is different from a prime-mortgage book or a BNPL lender’s queue — but the categories are stable.

1. Repayment-lifecycle events

Successful EMI, partial EMI, failed EMI, mandate bounce (NACH return / direct-debit reject), prepayment, scheduled foreclosure, interest accrual, charge posting. High volume, mostly automated by the LMS. The deterministic-core territory.

2. Repayment exceptions and disputes

Where the LMS and the borrower disagree about what happened.

- “I paid via UPI three days ago — your system still shows me as overdue.” (Payment-not-reflecting; intermediate-clearing lag, NACH file delay, partner-integration latency.)

- “I paid extra this month — please adjust against next EMI.” (Overpayment / excess-payment routing.)

- “Why was I charged a late fee? My EMI was on time.” (Disputed charges — late fees, bounce fees, prepayment charges, foreclosure charges.)

- “The interest rate revision wasn’t applied to my schedule.” (Interest disputes — rate, computation, floating-rate revisions.)

- “This transaction isn’t on my statement.” (Statement discrepancies.)

3. Borrower service requests

The vanilla self-service queue: statements, interest certificates, tax certificates (Form 16A in India, 1098 in the US), EMI-date change, repayment-mode change (NACH → standing instruction → UPI auto-debit), profile updates, channel-preference changes, beneficiary updates, foreclosure / prepayment quotes, NOC requests after closure, co-borrower / guarantor updates.

4. Disbursement queries

Post-disbursement tickets that are actually about the disbursement.

- “The amount hasn’t hit my account yet” (disbursement delay, holding-bank lag).

- “I expected the full sanction but only part disbursed” (partial / tranche disbursement, eligibility-condition gates).

- “It went to the wrong account” (account-detail mismatch, beneficiary-update failure).

- “What were these processing charges?” (disbursement-charge clarification).

5. Hardship and restructuring requests

“I lost my job, can I delay this month’s EMI?” “Medical emergency — can we restructure?” “Can I take a moratorium?” “Can the late fee be waived this once?” Mid-volume, high-judgment, policy-driven. The lender’s hardship policy defines the offer set; the question on each ticket is which offer applies, or whether to seek a non-standard exception.

6. Collections workflow

Pre-due reminders (T-3 to T-1), soft-bucket dunning (DPD 1–30), hard-bucket dunning (DPD 31–60), recovery escalation (DPD 60–90+), legal stage. Volume varies with portfolio quality; this is the workflow most consequential for the lender’s economics. The cadence, channel mix, and tone change as DPD increases — by DPD 60, the workflow is no longer “remind”, it is “negotiate” or “escalate”.

7. Complaints and disputes

Service complaints, fraud claims, unauthorised-debit claims, regulatory escalations (RBI Integrated Ombudsman in India, FCA DISP rules in the UK, CFPB complaint windows in the US), dispute resolution, NOC disputes, fee challenges. Low volume, high regulatory exposure, calendar-driven SLA pressure — missing a 30-day Ombudsman window costs more than the original dispute.

8. Compliance and periodic obligations

KYC re-verification cycles, AML / sanctions re-screening, document expiry (insurance, identity, employer letters), interest-rate revision notices, periodic disclosures, regulator-mandated borrower communications, co-borrower / guarantor verification refreshes. Calendar-driven, policy-bounded, audit-watched.

9. Operational exceptions

Settlement mismatches, integration timeouts, partner reconciliation failures, data discrepancies, pending approval queues, manual-intervention backlogs. The endless tail every LMS produces. Categories shift faster than rule-based automation can keep up with.

10. Lifecycle transitions

Top-up requests, loan closure, foreclosure booking, NOC issuance, NPA classification, restructured-asset accounting, write-off processing, recoveries against written-off accounts, insurance closure / portability, post-closure tax-certificate generation. Lower volume than the rest, but each one is high-stakes for ledger correctness — a wrongly closed loan or a misclassified NPA shows up in a regulatory exam.

That is the surface area. Ten categories, varying volumes, varying decision complexity, varying regulatory exposure. Any AI strategy for servicing has to live somewhere on this map.

What “agent” means in this context

Before mapping where agents help, three quick distinctions:

- Not a chatbot. A chatbot answers a borrower’s question; an agent runs the workflow the question implied. A borrower asking “can I delay this month’s payment?” doesn’t want an FAQ — they want a hardship offer routed through policy.

- Not RPA. RPA repeats fixed scripts on rails. An agent reasons about which workflow applies, picks the policy-compliant path, and stops when policy says it should.

- Not a copilot. A copilot drafts something and waits for a human to send it. An agent sends it, logs it, and waits for the borrower’s reply.

The architectural anchor: agents sit above a deterministic core. They do not replace it. The core owns the truth — schedules, balances, NPA buckets, the audit log. The agent reads from the core, drafts decisions inside policy, writes back through governed APIs. (More on the layering →)

Where AI agents can actually help

Walking the ten categories with the agent overlay.

Agent-led today

(2) Repayment exceptions and disputes. Payment-not-reflecting reconciliation queries — the agent checks the cleared-but-unposted view, the partner integration’s delivery log, and the NACH presentation file, drafts the reconciliation explanation, and triggers re-presentation if policy permits. Overpayment routing inside policy. Charge and interest disputes classified, the underlying calculation re-pulled from the core, and a draft response generated. Fee waivers within policy bounds: agent-led; out of policy: human approval.

(3) Borrower service requests. The agent’s most natural territory. Statements and tax certificates generated on demand from the core. EMI-date changes within policy bounds. Repayment-mode changes routed through the mandate workflow. Foreclosure quotes computed from the deterministic schedule. NOC issuance triggered automatically once closure conditions are satisfied.

(4) Disbursement queries. The agent retrieves disbursement status from the core, checks holding-bank acknowledgement, classifies the issue, and either resolves the borrower’s question with the available data or escalates with a structured ticket to operations when the disbursement is genuinely stuck.

(5) Hardship and restructuring — triage and offer routing. The agent classifies the hardship category against policy (job loss, medical, natural-event, structural income change, fraud claim), retrieves the offer set the policy authorises, drafts the offer, and either sends it (if inside the agent’s authorisation envelope) or routes it to a human approver (if not). Non-standard or out-of-envelope offers stay human; everything that leads up to them is agent work.

(6) Collections — pre-due through DPD 30. T-3 to T-1 reminders, soft-bucket dunning at DPD 1–30, payment-plan offers from the policy’s pre-approved set. The agent runs the cadence, listens for hardship language in the reply, and hands off when it hears it.

(7) Complaints — intake, classification, routing, draft response. SLA clocks running, regulator-watching. The agent reads the complaint, classifies it (service / product / regulatory / fraud), pulls the relevant ledger and audit history, routes it to the right queue with a draft response and the deadline visible. A human approves and sends.

(8) Compliance — KYC re-verification, document collection, anomaly escalation. Calendar-driven, document-driven, policy-driven. The agent identifies borrowers entering the re-KYC window, runs the document-collection sequence, validates against the lender’s KYC policy, posts the renewed identity record to the core, and escalates anomalies — mismatched details, document-quality failure, sanctions-list hit — to compliance with evidence attached.

(9) Operational exceptions — triage and draft resolution. The agent reads the exception, looks at the audit history, applies the resolution policy, and either resolves it directly or escalates with a draft answer. The labour-saving is large because the queue is endless and category drift defeats rule-based automation.

Mixed — agent-assisted, human-led

(6) Collections at DPD 31–60 — transition zone. The agent keeps cadence and channel running, but the harder negotiations move to humans. The agent does the prep — pulling the borrower’s full history, the prior contact attempts, the policy-allowed offers, the regulator’s restrictions — so the human walks into the call already briefed.

(6) Collections at DPD 60+ and legal escalation. Once the loan is in recovery or legal phase, error consequences are non-recoverable. Wrong borrower contacted, wrong amount referenced, wrong notice issued — these become regulatory and reputational events. The right design is human-led with agent-drafted artefacts and full audit support, not the reverse.

(10) Lifecycle transitions. The agent drafts the borrower communication, prepares the application, validates the closure / top-up / NOC conditions. The booking itself runs through the deterministic core’s governed APIs, with human approval where policy requires it.

Belongs on the deterministic core, not the agent

(1) Repayment-lifecycle event posting itself. Interest accrual, repayment allocation, NACH presentation, schedule revision after partial payment — pure determinism. The core does this; there is no reasoning for an agent to do.

(10) NPA classification, restructured-asset accounting, write-off processing. Deterministic by regulatory mandate. Under RBI’s IRACP norms, IFRS 9, or CECL, classification is a pure function of inputs, time, and policy version. Reading those inputs probabilistically introduces non-reproducibility no auditor will accept. The deterministic core does this. Always.

The map at a glance

How to deploy this without breaking trust

Knowing where agents help is half the answer. The other half is the platform underneath. Four properties separate an agent deployment that survives the regulator’s first audit cycle from one that doesn’t. Treat them as deployment steps, not aspirations.

Step 1: Put a deterministic core under everything

The agent does not own the truth. The truth lives in a deterministic ledger the agent reads from and writes through. Schedules, balances, NPA classification, the audit log — none of it lives in agent state. This sounds obvious; the reason it isn’t is that early agent platforms shipped with their own state machines for “speed of deployment,” and regulators are now finding deployments where the agent’s view of the loan and the LMS’s view diverged. Don’t be that lender.

Step 2: Treat policy as code, not policy as prompts

The hardship-offer envelope, the dunning cadence, the escalation thresholds, the channel rules, the fee-waiver authorisation table — these are policy. Policy goes in a versioned policy engine the agent calls into, not into the agent’s prompt template where it is invisible to compliance and gets overwritten on the next iteration. Every agent decision links by reference to the policy version it evaluated against. When policy changes, agent behaviour changes — without a re-deployment, and with the change recorded as a policy event.

Step 3: Enforce the authorisation envelope at the API boundary

Inside the agent’s authorisation envelope, the agent acts. Outside it, the agent stops and escalates. The envelope is enforced by the platform, not by the agent’s training — there is no prompt attack that gets the agent to authorise a discount it isn’t allowed to authorise, because the discount is rejected at the API boundary, not at the prompt boundary. This is what distinguishes an agent platform from “an LLM with tool calls.”

Step 4: Make the audit log identical in shape to a human’s

Every action an agent takes — message sent, offer drafted, ledger entry posted, exception resolved — produces an audit record indistinguishable in structure from the equivalent human action, attributed to the agent identity. When a regulator asks for the methodology trail behind a specific decision, the lender produces it without explaining “but the agent did this so we have a different format.” There is no different format.

If your agent platform doesn’t satisfy all four, the servicing automation has an expiry date. The expiry is the next audit.

How Lokta implements all four

Lokta’s AI loan servicing is our agent platform for loan servicing. The four properties above are architectural defaults, not configuration:

-

Deterministic core. The servicing agent runs on top of Lokta’s loan-management core, the deterministic ledger of record. The agent reads from the ledger, writes through its governed APIs, and never holds its own copy of the borrower record. The ledger and the agent cannot disagree because they are not separate systems.

-

Policy as versioned code. Lender policies — hardship envelopes, dunning cadences, complaint SLAs, escalation thresholds, channel rules, fee-waiver tables — are configured in Lokta’s policy engine and versioned alongside the rest of the platform. Every agent decision links to the policy version it ran against. When policy changes, agent behaviour changes; the change is auditable as a policy event.

-

Authorisation envelopes at the API boundary. Servicing agents operate inside an envelope enforced at Lokta’s API boundary, not at the model boundary. An agent attempting an out-of-policy action receives a structured rejection. No prompt-engineering route around it, because the model never gets the chance to try.

-

One audit log. Human servicing actions and agent actions are logged in the same schema, queryable by the same tools, exported through the same regulator interfaces. When the audit committee asks for a trail, “human or agent” is a column, not a different report.

The pattern that’s working in the field with our design partners is the one this post described: start where volume × policy-clarity is highest — borrower service requests, repayment exceptions, disbursement queries, pre-due and soft collections, exception triage. Hardship triage, complaints, and compliance follow once the playbook is bedded in. NPA classification and lifecycle ledger transitions stay where they belong — on the deterministic core. Late-stage collections stay in human hands, agent-assisted.

If you are evaluating where to start an AI servicing programme, the question is less which platform than which category. The platform decision follows from getting that one right.

Read next:

- AI in lending — the deterministic core — why an agent layer is only as trustworthy as the core under it.

- Agentic Lending and the 5× Problem — the throughput and observability math no one is doing on agentic operations.

- Lending glossary — the twelve terms that recur across this post defined in 100 words each.

Frequently asked questions

What is loan servicing?

Loan servicing is the operational layer of lending that runs from disbursement until the loan is closed — paid off, foreclosed, written off, or settled. It covers schedule generation, repayment processing, interest accrual, charges, borrower communication, hardship handling, collections, NPA classification, regulatory reporting, complaint resolution, and lifecycle events such as top-ups, closures, and write-offs. Servicing is the longest phase of the loan lifecycle (typically 90–99% of its calendar life) and the phase where the lender’s economics actually realise.

What types of tickets arrive in a loan servicing operation?

Ten categories. Repayment-lifecycle events (EMIs, prepayments, foreclosures); repayment exceptions and disputes (payment-not-reflecting, overpayment, disputed charges and interest); borrower service requests (statements, tax certificates, foreclosure quotes, NOCs, EMI-date changes); disbursement queries (delays, partial disbursement, tranche timing); hardship and restructuring; collections workflow (pre-due through legal escalation); complaints and disputes; compliance and periodic obligations (KYC, sanctions, document expiry, rate revisions); operational exceptions; and lifecycle transitions (top-ups, closure, NPA, write-offs). The mix varies by lender; the categories are stable.

Which loan servicing tickets can AI agents handle today?

Seven of the ten categories are agent-led territory: repayment exceptions and disputes (payment-not-reflecting reconciliation, overpayment routing, charge and interest classification with policy-bounded resolution); borrower service requests (statements, tax certificates, foreclosure quotes, NOCs, EMI-date changes); disbursement queries (status retrieval, delay escalation); hardship triage and offer routing (with human approval for non-standard offers); pre-due to DPD 30 collections; complaint intake and routing; compliance and periodic obligations; and operational-exception triage.

Which loan servicing tickets should NOT be handed to AI agents?

Three categories stay off the agent layer. Repayment-lifecycle event posting itself (interest accrual, allocation, NACH presentation) is pure determinism and lives on the deterministic core. NPA classification, restructured-asset accounting, and write-off processing are deterministic by regulatory mandate. Late-stage collections (DPD 60+) and legal escalation are human-led with agent-drafted artefacts because error consequences are non-recoverable. Lifecycle ledger transitions (closure, top-up booking, NOC issuance) run through the core’s governed APIs; agents draft borrower communication only.