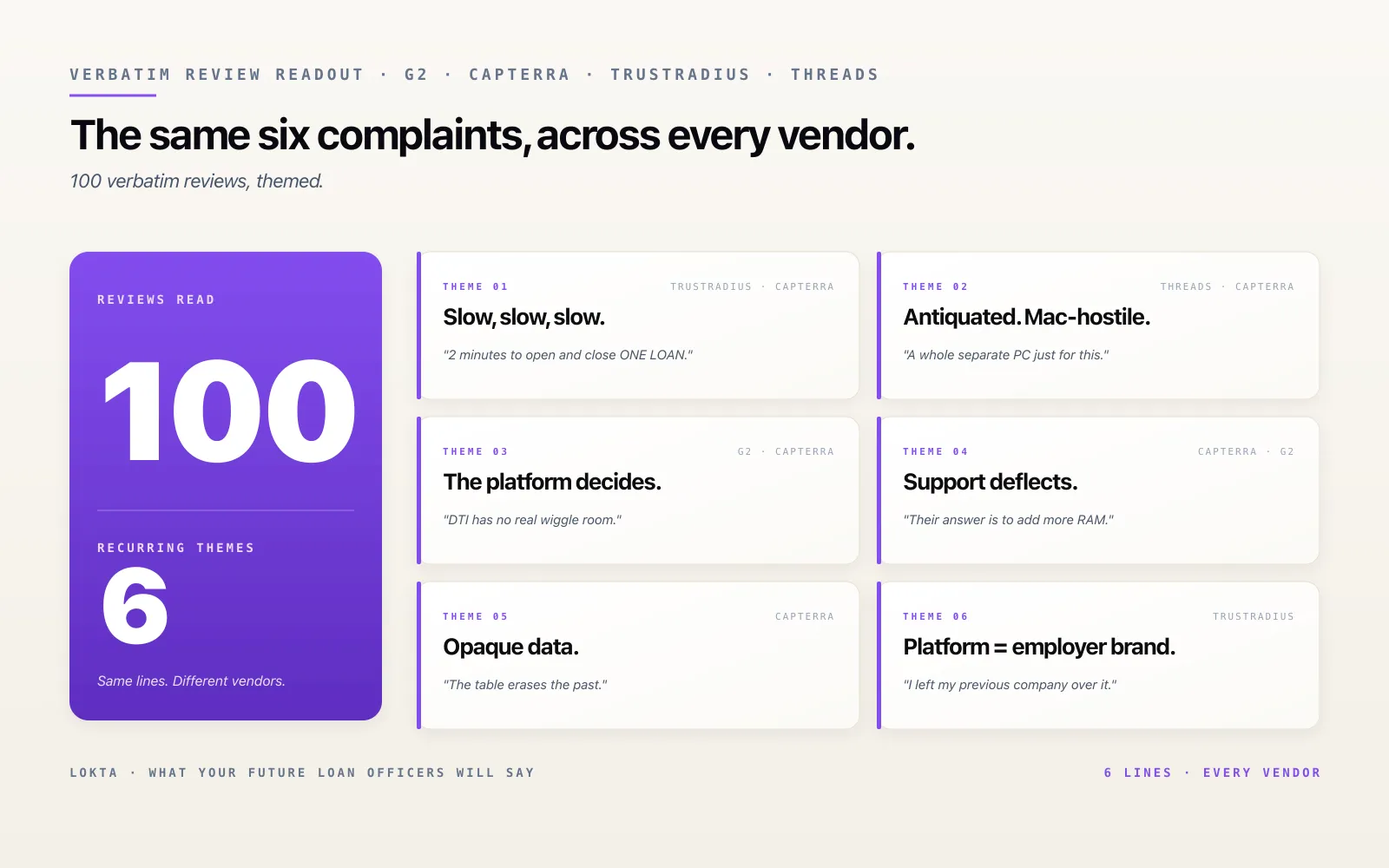

100 LMS Reviews — The Same Six Complaints Recur

We read 100+ public LMS and LOS reviews from loan officers and servicers. The same six complaints recur across every vendor — here is the theme-by-theme map.

A Loan Management System (LMS) — also called a loan servicing platform, and in its origination-side cousin, a Loan Origination System (LOS) — is the software a lender’s loan officers, processors, underwriters, and servicing agents touch every day. It is the difference between a loan that funds in seven days and one that funds in twenty-one. It is also, judging by the public review record, the single most resented piece of software in the modern lender’s stack.

Over the last several weeks we read through more than one hundred verbatim reviews of the most-deployed Loan Management Systems and Loan Origination Systems in the United States and globally — the dominant US Home Loan LOS, a long-tenure mortgage LOS, the dominant commercial banking LOS, two consumer-lending LOS platforms, a consumer-loan servicing platform, and a global digital-lending platform — across G2, Capterra, TrustRadius, Software Advice, and Threads. We did not look for the worst quotes. We looked for the recurring ones. The pain rhymes across every platform.

This post is a structured round-up of those verbatim reviews, grouped by theme, with attribution and source URL on every line so you can verify the originals. Brand names have been replaced with descriptive platform labels — the pattern is architectural, not product-specific, and the framing should reflect that. The language inside the quotes is otherwise the way frustrated practitioners sound when they think no one important is listening.

If you are evaluating an LMS or LOS, this is the unfiltered language your future loan officers, processors, and admins will use about whatever you choose. If you are an executive being told your incumbent platform “works fine,” this is what your team is saying about it on the public internet.

- Six lines surface across every vendor. Slow. Antiquated. The platform decides. Support deflects. Data is opaque. The platform is part of the employer brand.

- The pattern is the architecture, not the product. Fragmented modules, vendor-controlled schemas, batch-refreshed state, and services-led customization are common to the entire previous generation of lending software.

- Operational cost. A two-minute open/close per loan, repeated through a working day, is the difference between a processor closing thirty files and closing fifteen.

- Strategic cost. Hard-coded DTI ranges and rigid underwriting parameters outsource credit policy to the vendor’s release calendar.

- Talent cost. A Loan Management System is now part of a lender’s employer brand. Loan officers actively filter their next employer by which LOS the lender runs.

Theme 1 — “Slow, slow, slow”

The single most frequent complaint across every Loan Management System we surveyed is speed. The verbatims are blunt.

“Windows 95, slow, slow, slow.”

— Capterra reviewer, the dominant US mortgage LOS.

“It takes about 2 minutes to open and close ONE LOAN.”

— Loan officer, the dominant US mortgage LOS (Capterra).

“[The platform] has a reputation for crashing at least once or twice every couple of weeks, and since there is no auto save, this wreaks havoc and slows the process way down, resulting in lost referral business and turnover.”

— TrustRadius reviewer, the dominant US mortgage LOS.

The lending consequence of those numbers is not abstract. A two-minute open-and-close on a single loan, repeated across a working day, is the difference between a processor closing thirty files and closing fifteen. A Loan Management System that crashes “at least once or twice every couple of weeks” without autosave does not lose seconds — it loses referral business, by the reviewer’s own words.

Theme 2 — Click-heavy, antiquated, Mac-hostile

Speed complaints overlap with a second theme: the platform was designed for a workflow no modern loan officer recognises. One Threads post made the rounds in late 2025:

“[The platform] does not have a Mac version. I find this so unacceptable in 2025. The web version is also separate and my licensing company doesn’t provide it. Only the resident software program. This is so antiquated. I literally have to have a whole separate PC for this while all my other work is done on the Mac systems I’ve used for the last 10 years. How do I even use a PC?”

— Loan officer @justchellebell on Threads, describing the dominant US mortgage LOS.

For a long-tenured user of a different mortgage LOS, fifteen years of accumulated frustration produced perhaps the most-cited review-site sentence in this category:

“After 15 years of using [it] I have never hated a company as much as I do now.”

— Capterra reviewer, a long-tenure mortgage LOS.

These are not edge-case grievances. They show up in lender exit interviews. They show up in the labour market — loan officers actively filter their next employer by which LOS the lender runs.

Theme 3 — The platform decides, the lender obeys

A different kind of frustration shows up among admins and operations leads: the Loan Management System is opinionated, and not in their favour. The system’s underwriting parameters, ratios, and field labels cannot be reshaped to fit the lender’s policy.

“The ratios and underwriting criteria within the platform were not flexible to institutional needs, with the DTI as [the vendor] coded it having no real wiggle room and not being changeable by customers and administrators themselves.”

— G2 reviewer, a consumer-lending LOS.

“Everything has to be done the way [the platform] wants it to be done as opposed to creating a custom experience/approach that fits your organization’s needs.”

— Capterra reviewer, a consumer-lending platform.

“The end client experience is clunky, and the system was built for bank staff rather than from the end client perspective.”

— G2 reviewer, the dominant commercial banking LOS.

The DTI complaint is the one that should worry a Chief Credit Officer most. A debt-to-income ratio is a credit-policy decision, not a software decision. When the LMS hard-codes it and the institution cannot change it, the institution is, in effect, outsourcing credit policy to a vendor’s release calendar.

Theme 4 — Customer support deflects, dismisses, or disappears

A theme so consistent across vendors it deserves its own section.

“Customer support’s default reply is ‘no one else has complained’ until they realize it is a wide spread issue and only then do they take any sort of half hearted action.”

— Capterra reviewer, the dominant US mortgage LOS.

“Regardless of the issue, their answer is to add more RAM.”

— Capterra reviewer, the dominant US mortgage LOS.

A reviewer aggregation summarising deployments of a different platform captured the pattern in a single line:

“The management completely ignores complaints, points fingers at clients.”

— Reviewer summary across Capterra and G2, a global digital-lending platform.

The procurement implication is direct. An RFP for a Loan Management System should not stop at “describe your support model.” It should ask vendors to provide three references whose tickets were resolved in under five business days in the last quarter, and to commit to a contractual SLA on first-response time and time-to-resolution for severity-1 lending-impact incidents (a failed disbursement run, a borrower-statement generation outage, an NPA-flag misclassification).

Theme 5 — Data is structured for the vendor, not for the lender

This is the theme that hurts most when the lender tries to graduate to portfolio analytics, governed AI, or a regulator-grade audit.

“The way data is structured is convoluted and opaque… which can be frustrating for data analysts. When modifying a loan, the table loan_reverse_status_archive erases the past, which is problematic for accounting.”

— Capterra reviewer, a consumer-loan servicing platform.

“The system does not record attempted payments with debit cards, so users have no idea if and how frequently payments are failing.”

— Capterra reviewer, a consumer-loan servicing platform.

A loan modification that erases history is not a UX problem. It is a books-and-records problem the moment an examiner asks for the reasoning behind a status change. A payment-attempt blind spot is not a UX problem either — it is the silent precursor to a portfolio-level delinquency surprise.

Theme 6 — The most-quoted line in lending-software marketing

Across all the verbatims we read, one line is being lifted into more competitive pitch decks than any other:

“I left my previous company over [the dominant US mortgage LOS], and will only work for lenders who do not utilize [it] as their LOS.”

A Loan Management System is no longer a back-office tool. It is part of a lender’s employer brand. The talent market is small enough — mortgage processors, commercial underwriters, collections specialists — that platform reputation circulates faster than a recruiter can move.

What lenders should ask in an RFP

A buyer-grade Loan Management System RFP, framed against the verbatims above, should require vendors to demonstrate evidence — not promises — against each of the six themes. One ask per theme.

A documented average open/close time per file under realistic load, with autosave enabled by default. No “the system is fast” demos — ask for a measured p95 and the methodology that produced it.

Native browser-based access from macOS, Windows, and Linux without a separate “thick client.” A loan officer should not need a second computer to use the LMS.

DTI ranges, LTV thresholds, ratio overrides, and score cutoffs changeable by the lender’s risk team — without a vendor SOW. Credit policy is the lender’s job, not the vendor’s release calendar’s.

A contractual SLA on first-response and time-to-resolution for severity-1 lending-impact incidents — failed disbursement runs, statement-generation outages, NPA-flag misclassification.

A non-destructive audit trail of every loan-state change (including reversed modifications) and a queryable record of every payment attempt — successful, failed, retried. The system of record cannot also be the system that forgets.

Two reference customers willing to speak about support-escalation experience in the last twelve months, plus three references whose severity-1 tickets resolved in under five business days last quarter.

The verbatims in this post are the language those reference customers will actually use. A buyer who reads the reviews before the demo will not be surprised by what they hear.

A closing observation

Every Loan Management System will have detractors on a public review site; that is a fact about software, not about LMS specifically. What is striking about lending-platform reviews is the consistency of the language across vendors and across years. “Slow.” “Antiquated.” “The platform decides.” “Support deflects.” “Data is opaque.” When the same six lines surface across six otherwise-different products, the pattern is not the product. The pattern is the architecture — fragmented modules, vendor-controlled schemas, batch-refreshed state — that the entire previous generation of lending software was built on.

The next architecture of lending systems will be judged by whether its public review record reads differently five years from now.

Frequently asked questions

Why does the same complaint show up across every LMS and LOS vendor?

Because the pattern is architectural, not product-specific. Fragmented modules, vendor-controlled schemas, batch-refreshed state, and services-led customization are common to the entire previous generation of lending software. When six complaints — slow, antiquated, inflexible, support-deflects, opaque data, platform-as-employer-brand — surface across six different vendors, the pattern is not the product. The pattern is the architecture underneath all of them.

What should a buyer ask in an LMS or LOS RFP after reading these reviews?

A buyer-grade RFP, framed against the verbatims, should require vendors to demonstrate evidence for: documented average open/close time per file under realistic load with autosave on by default; native browser-based access from macOS, Windows, and Linux without a separate thick client; an admin-configurable credit-policy layer (DTI, LTV, ratios, score cutoffs) changeable by the lender’s risk team without a vendor SOW; a non-destructive audit trail of every loan-state change; tracked outcomes for every payment attempt; a contractual SLA on response and resolution for lending-impact incidents; and two reference customers willing to speak about support escalation experience in the last twelve months.

Why are the editorial attributions stripped of brand names?

Brand identification is not the point of this post — the recurring pattern is. Public reviews on TrustRadius, Capterra, G2, Software Advice, and Threads are linked in the sources list so readers can verify any quote against its original review page. The editorial framing uses descriptive platform labels (dominant US mortgage LOS, dominant commercial banking LOS, long-tenure mortgage LOS, etc.) so the focus stays on the architectural pattern, not on individual vendors.

How is this post different from the Lending Technology Pain Map?

The Pain Map cuts the same source material by audience — what loan officers, in-house tech teams, and executives each say about the same platform. This post cuts it by complaint theme — the six lines that surface across every vendor regardless of who wrote the review. Both posts share a sources base; the framing answers different buying-committee questions. Read the Pain Map for the territory; read this post for the unfiltered language your future loan officers will use about whatever you pick.

Where do the 100 reviews come from?

G2, Capterra, TrustRadius, Software Advice, and Threads. Coverage spans the most-deployed Loan Management Systems and Loan Origination Systems in the United States and globally, including the dominant US Home Loan LOS, the dominant commercial banking LOS, a long-tenure mortgage LOS, two consumer-lending LOS platforms, a consumer-loan servicing platform, and a global digital-lending platform. Every quote in the post is linked to its source page.

Read next:

- The Lending Technology Pain Map: 3 Audiences — the same source material cut by audience. Loan officers, in-house tech, and executives describe the same platform in three different vocabularies.

- Every Lender Replaces Their LMS Eventually — five symptoms tell you whether you replace your LMS on your terms or the board’s. Three or more on the table is a board-level risk, not an IT one.

- Why lender portfolio analytics lives in Excel — the structural reason portfolio analysis migrates out of the LMS and into spreadsheets.

- The LMS customization trap — why every non-standard need on a legacy LMS becomes a priced vendor project.

- The LMS RFP toolkit — turn these review-grade questions into a running RFP: a vendor-neutral checklist, 50 vendor questions, a scorecard, and security and AI-governance questionnaires.

Sources:

- Capterra — the dominant US mortgage LOS reviews

- TrustRadius — the dominant US mortgage LOS reviews

- Threads — loan officer @justchellebell on the Mac/PC requirement

- Capterra — a long-tenure mortgage LOS reviews

- G2 — the dominant commercial banking LOS reviews

- G2 — a consumer-lending LOS reviews

- Capterra — a consumer-lending platform reviews

- Capterra — a consumer-loan servicing platform reviews

- Capterra — a global digital-lending platform reviews

- G2 — a global digital-lending platform reviews

Ashok Auty is the co-founder of Lokta and co-creator of Apache Fineract. He has spent two decades building lending infrastructure and reads every public LMS review surface he can find — because the recurring lines tell you what the architecture, not the brand, is doing to the people who use it every day.